Banks’ IT adoption and lending all through the pandemic

The escalating adoption of electronic innovations in the economical system is pushing the tutorial discussion about its probable added benefits or negatives to appear for a reliable foundation of empirical evidence. Though prior studies have investigated the outcomes of details engineering (IT) adoption on diverse banking outcomes (e.g. Beccalli 2007, Koetter and Noth 2013), results so much have been inconclusive and, apart from a couple of exceptions (Pierri and Timmer 2020, Kwan et al. 2021), have not however been analyzed for the duration of intervals of crisis.

In our latest paper (Branzoli et al. 2021), we exploit the Covid-19 pandemic – an unpredictable celebration that is most likely to have enhanced the worth of electronic prowess as a source of aggressive edge – to analyse variants in credit history throughout Italian banks connected with unique ex-ante stages of IT adoption. We obtain that IT-intensive financial institutions improved their lending to non-money firms (NFCs) additional than other individuals in the months following the outbreak of the pandemic the maximize was economically sizable even when nationwide mobility limitations have been lifted and community overall health situations enhanced.

Measuring banks’ IT adoption

We measure banks’ amount of IT adoption working with distinctive knowledge on IT-related expenses documented in the earnings statement and survey details on the use of digital technologies at the financial institution level. These are expenses incurred for the purchase of hardware (e.g. private pcs, servers, mainframes) or computer software, the compensation of IT professionals (e.g. computer system aid engineers) and the outsourcing of IT services to external vendors. IT fees are normalised by the whole functioning prices of the lender. Determine 1, Panel A, shows the evolution of the IT-to-whole costs ratio in excess of time and throughout percentiles.

To evaluate irrespective of whether a larger share of IT prices is similar to a better degree of IT adoption, we take a look at the relationship involving banks’ IT expenditures and the use of digital systems. We mix knowledge on IT charges with financial institution-stage survey facts on the status of electronic transformation of the Italian banking sector.1 More especially, we inquire banking institutions to reveal which monetary providers they present on the internet (e.g. loans, payments, asset administration), if any. Respondents are also requested whether they have revolutionary jobs below way, which know-how underlines them (e.g. major information, biometrics, synthetic intelligence) and for what intent (for occasion, bettering client profiling or credit rating hazard evaluation). Managing for a wealthy established of financial institution properties (which include size, funding composition, and profitability), we uncover that our evaluate of IT adoption is basically related to banks’ degree of digitalisation and propensity to innovate: the bigger the IT expenses, the larger the likelihood of giving electronic solutions and partaking in progressive processes.

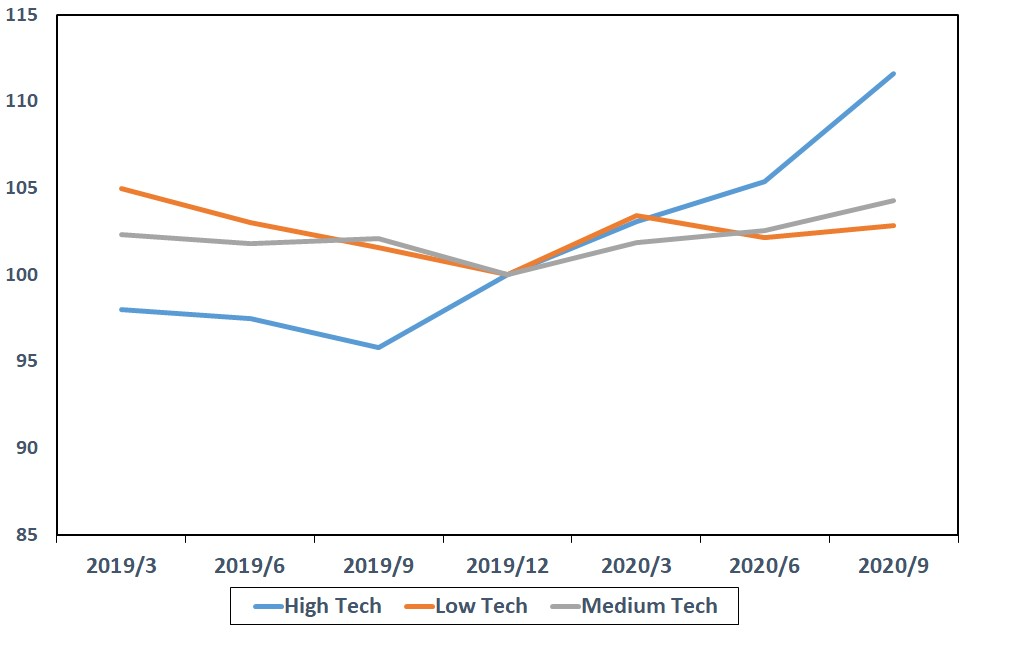

Panel B of Determine 1 displays credit dynamics in Italy in advance of and after the pandemic outbreak, based on banks’ diploma of digitalisation: since the beginning of 2020 credit history drawn by higher tech banking companies (i.e. these in the major quartile of the distribution of the IT-to-whole fees ratio) greater by 11%, 2 times the fee recorded by other loan providers.

Figure 1 IT costs distribution (Panel A) and credit history dynamics throughout banks’ tech stages (Panel B)

Panel A

Panel B

Notes: The top graph shows the evolution of the 25th percentile, the median, and the 75th percentile of the distribution of the IT-to-complete expenses ratio in each individual 12 months. The bottom graph displays lending designs across banks with various degrees of IT adoption. All banking institutions in our sample are split into 3 groups according to their IT-to-complete prices ratio: lower tech if they slide in the bottom quartile, medium tech if they stand concerning the second and 3rd quartile and, substantial tech if they are in the major quartile. The total quantity of credit rating for each each and every lender is normalised to 100 based mostly on the quantity of exceptional credit score in December 2019.

Credit rating allocation

We also investigate the dynamics of credit score and its allocation across NFCs. Making use of a big difference-in-dissimilarities identification system, we obtain that the effect of IT on credit rating development was much larger for borrowers hardest hit by the pandemic. NFCs located in the areas of the region most influenced by the pandemic2 experienced a higher boost in lending from bigger-tech loan companies. We obtain positive variation in credit score for enterprises operating in sectors considered non-crucial all through the lockdown and for that reason compelled to close their bodily areas. Little and medium-sized enterprises (SMEs) – much more exposed than bigger companies to liquidity shortfalls – have benefited the most from the growth in loans fuelled by technologically highly developed financial institutions.

Electronic versus actual physical channels

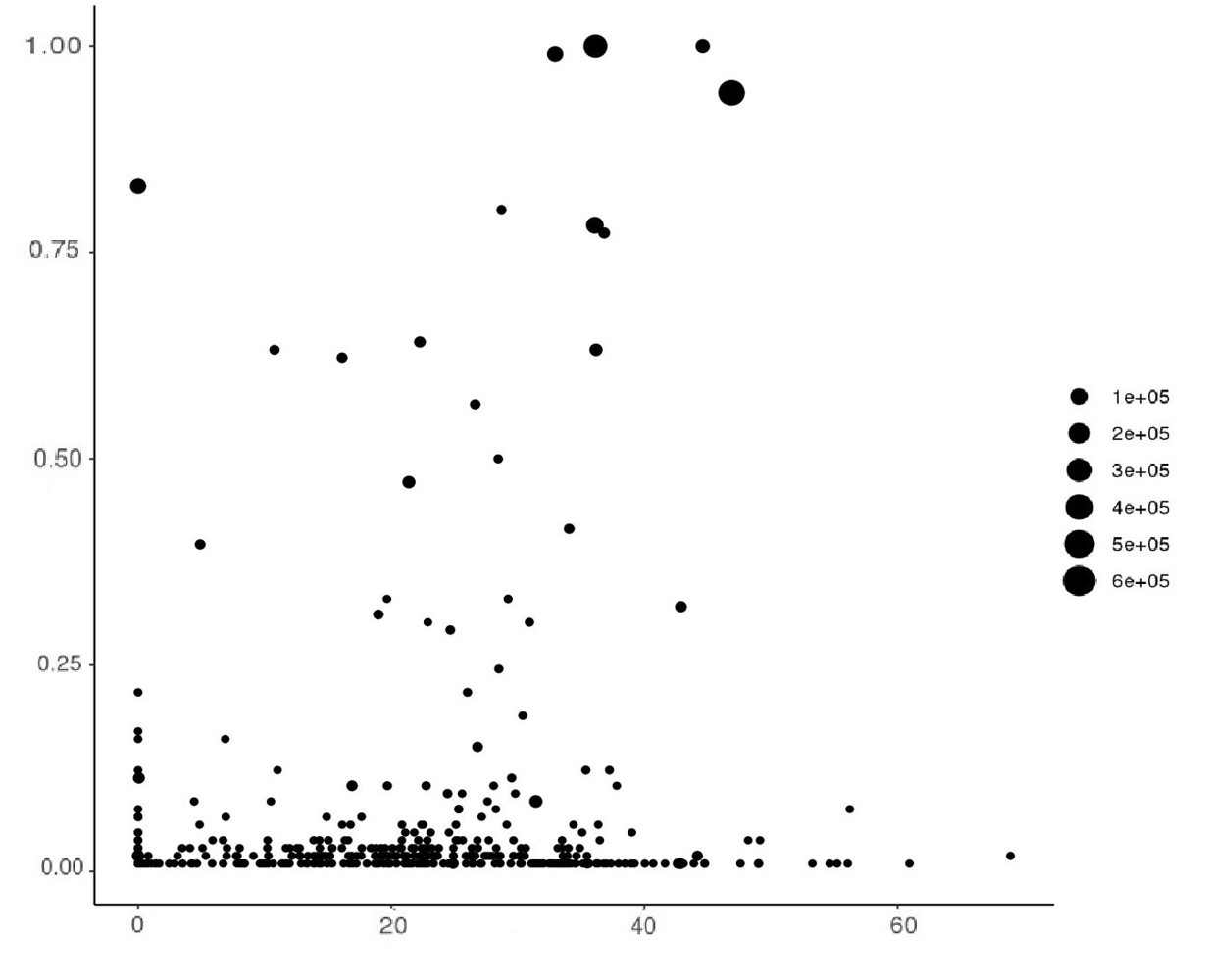

Regardless of whether technological innovation is reducing the result of length on lending conclusions is below discussion (Petersen and Rajan 2002, Basten and Ongena 2020, Keil and Ongena 2020). In our assessment, we study the job of geographic proximity (in between creditors and debtors) in influencing the outcome of technologies adoption on credit for the duration of the pandemic. Determine 2 plots the actual physical and electronic get to of Italian financial institutions at the eve of the pandemic: at comparable technological levels, the dispersion of department diffusion reflects a large heterogeneity in banks’ organization products. In exploring the relative worth of these two dimensions, we find that banking institutions capable to provide their prospects via both equally conventional and electronic channels showed the maximum credit score advancement from March 2020 onwards in other terms, we deliver proof that brick-and-mortar areas even now matter, when blended with a strong digital existence of the bank.

Determine 2 Distribution of physical as opposed to electronic channels

Notes: The horizontal axis reveals the IT expenditures ratio. The vertical axis presents the percentage of provinces in which the lender has a department. Size of dots correspond to overall belongings in millions of euro. All computed in 2020.

Conclusion

We get rid of gentle on the effects of technologies adoption in lending during the Covid-19 pandemic. Our effects propose that banking companies with a increased diploma of pre-pandemic IT adoption have granted additional credit history to NFCs as the crisis started to unfold. Bigger digital abilities may well have assisted banking institutions handle a bigger-than-common amount of financial loan purposes, strengthen workflow by automation, and streamline acceptance processes. We also show that, even underneath serious bodily limits, buyers even now valued the probability of acquiring experience-to-encounter interactions with their bank. Our analysis paves the way for long run investigation on the long-term repercussions of digitalisation in banking. As the pattern in the direction of digital uptake is below to stay, financial institutions have to have to adapt to modifying buyer tastes and foresee shifts in competition. Implications for enterprise design innovation will undoubtedly lie forward.

Authors’ be aware: The sights expressed here are all those of the authors and do not automatically mirror these of the Financial institution of Italy.

References

Basten, C and S Ongena (2020), “Online home finance loan platforms can make it possible for tiny financial institutions to increase their inter-regional diversification”, VoxEU.org, 15 August.

Beccalli, E (2007), “Does IT investment boost bank performance? Evidence from Europe”, Journal of Banking & Finance 31(7): 2205-2230.

Branzoli, N, E Rainone and I Supino (2021), “The role of banks’ technology adoption in credit score markets during the pandemic”, Working Paper.

Keil, J and S Ongena (2020), “It’s the conclude of financial institution branching as we know it (and we feel high-quality)”, Working Paper.

Koetter, M and F Noth (2013), “IT use, efficiency, and current market electricity in banking”, Journal of Financial Balance 9(4): 695-704.

Kwan, A, C Lin, V Pursianen and M Tai (2021), “Stress testing banks’ digital capabilities: Proof from the covid-19 pandemic”, Performing Paper.

Petersen, M and R Rajan (2002), “Does length however subject? The information revolution in compact company lending”, Journal of Finance 57(6): 2533-2570.

Pierri, N and Y Timmer (2020), “Tech in Fin just before FinTech: The worth of technologies in banking for the duration of a crisis”, VoxEU.org, 9 August.

Endnotes

1 The Regional Lender Lending Study (RBLS), performed by the Lender of Italy on a yearly basis, requires a large sample of Italian banking institutions symbolizing 90% of the deposits of the whole banking process.

2 The severity of the pandemic is tracked employing knowledge on hospitalisations, deaths, and modifications in residential mobility at the province stage.