")

Progress Software: Don’t Overlook The Growth Options (NASDAQ:PRGS)

Source: Progress Software

Progress Software (NASDAQ:PRGS) is demonstrating signs that it can rejuvenate its growth factor in the competitive space for application development platforms. Its balanced factor grades will improve sentiments heading into CY’21, given the weak momentum factor in 2020. Overall, Progress’s solid financials provide the optionality to improve the prospect of its platform.

Demand

Source: Seeking Alpha

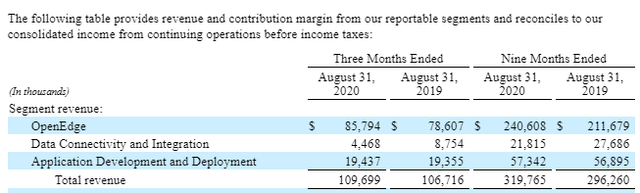

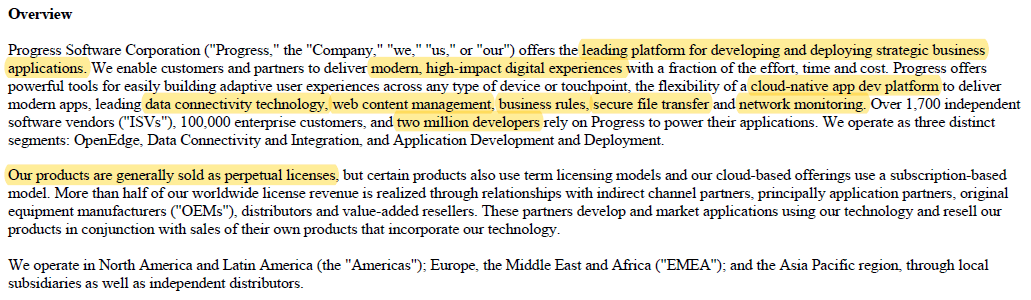

Progress Software is a PaaS (platform-as-a-service) business. It operates three segments, namely OpenEdge, Data Connectivity & Integration, and Application Development & Deployment. OpenEdge is the largest segment. OpenEdge is also the segment recording the best growth. The strong growth has benefitted from recent acquisitions. This trend is expected to continue given Progress Software’s focus on its M&A strategy to drive growth.

The OpenEdge business segment drives growth within OpenEdge’s large, diverse partner base by providing the technology enhancements and marketing support these partners need to sell more of their existing solutions to their customers. The OpenEdge business segment is also focused on providing partners and direct end users with a clear path to develop and integrate cloud-based applications – Source – Progress

OpenEdge includes application development, business rule management, secure collaboration, predictive maintenance, file transfer, and network monitoring solutions. Some of these capabilities were derived from the recent acquisition of Ipswitch.

Progress has been around for a long time. This means its business strategy will tilt towards balancing growth and profitability. It is important to highlight this point because the valuation multiple and risk premium expected of Progress will differ from most new-generation tech stocks.

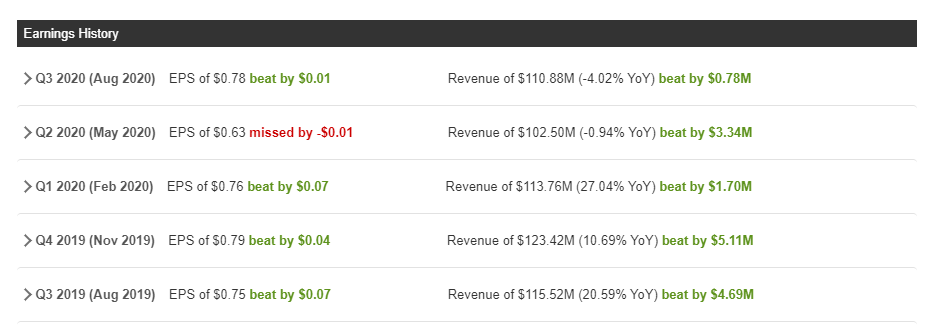

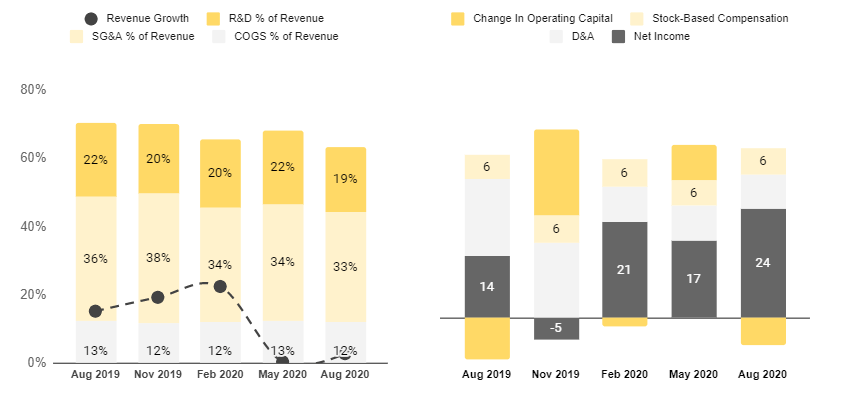

In recent quarters growth has been impressive before the pandemic led to a deceleration. The growth factor has benefitted from strategic acquisitions to extend the capabilities of its offerings.

Source: Seeking Alpha

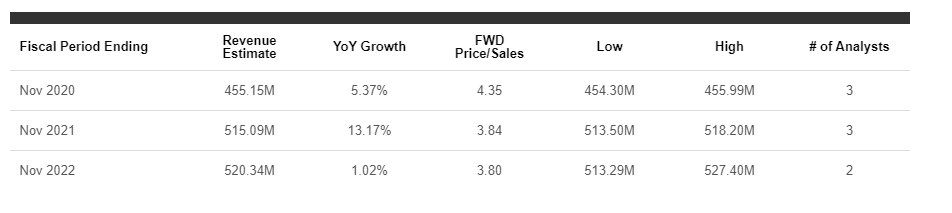

The boost to the growth grade explains the 13% growth projected for FY’21 in the table above. Last quarter, Progress highlighted its guidance to double revenue within the next five years. This implies sustained low-double-digit growth in the coming years. I find the guidance attractive given the huge competition that Progress has faced in most of its operating segments.

Business

Source: Progress

Source: Progress

Progress’s sales strategy combines its direct sales efforts and partnerships (SIs, resellers, developers). It is also important to highlight that Progress has a solid international presence. Progress recently announced its strengthened partnership with Ingram Micro to penetrate Iberia (includes Spain and Portugal).

On the product front, Progress is growing the capabilities of its platform to drive strong recurring revenue.

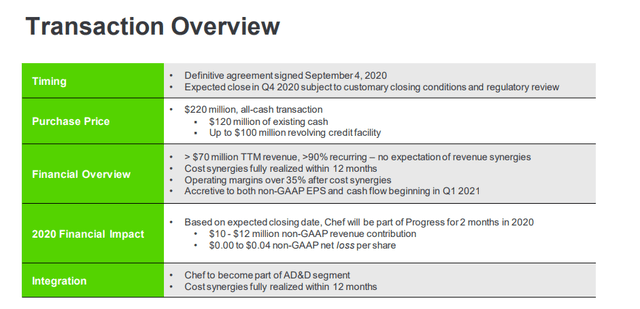

Founded in 2008, and with over $70 million in annual recurring revenue, Chef is a leader in continuous automation, an innovator in application automation and a pioneer of the DevSecOps movement.- Source – Progress

Recently, Progress acquired Chef. Chef adds capabilities in DevOps and DevSecOps. Chef complements Progress Software’s strategy of driving recurring revenue, and it is expected to be immediately accretive to growth and earnings.

Source: Author (using data from Seeking Alpha)

Progress has solid gross margins. This is a key factor driving its attractive profitability grade. It is also impressive to know that OpEx % of revenue has improved y/y. The last couple of quarters gained from cost savings related to less travel and marketing expenses. Progress is also conducting cost optimization initiatives. These developments are driving earnings. The improved earnings are flowing to the OCF line. This has allowed Progress to pay dividends and conduct a share buyback program. These activities are increasing the total return to shareholders. The sustainability of the buyback and dividend program also benefits from Progress Software’s decision to raise debt to fund its recent acquisitions. The cost of debt won’t offset its capital structure, given its strong EBITDA growth. This means Progress can easily fund future acquisitions with cash without diluting shareholders.

Given that Progress has been able to balance growth and profitability, the addition of Chef will rejuvenate the growth story heading into 2021. Going forward, it is important to explore the competitive posture to determine the sustainability of cash flow growth given the macro headwinds to the top line.

Competitors

Source: Progress

Progress is positioned as a platform. This means it can benefit from the integration of new capabilities. Some of these capabilities might play into hot tech trends resulting in a rejuvenation of the growth factor if Progress can find a solid competitive differential.

Progress Software’s capabilities in network monitoring, business rules, and secure file transfer are attractive. This will be complemented by its move into the DevSecOps space via the acquisition of Chef.

In its annual report, Progress highlighted the strong competition from players such as Microsoft (NASDAQ:MSFT), Amazon (NASDAQ:AMZN), IBM (NYSE:IBM), and Oracle (NYSE:ORCL).

Source: Gartner

Chef Software is stronger than most of its competitors at compliance support, vulnerability management support, and community ecosystem. It’s average at discovery and orchestration and weaker at model creation and editing. – Source – Forrester

The acquisition of Chef will boost Progress’s competitive posture. Chef was named in Forrester’s analysis of infrastructure automation platforms. It got a solid score for its governance and compliance capabilities. As a strong contender, its rank will be significantly boosted by Progress’s sales network given its low score in “market presence.” Chef already boasts of over 700 paying customers, including many Fortune 500 companies. Progress highlighted Chef’s strong open source community in the acquisition update call, which has driven over 40 million downloads. Chef will be added to the AD&D segment providing the much-needed support for OpenEdge, which has done the bulk of the heavy lifting to drive growth.

Source: Progress Software

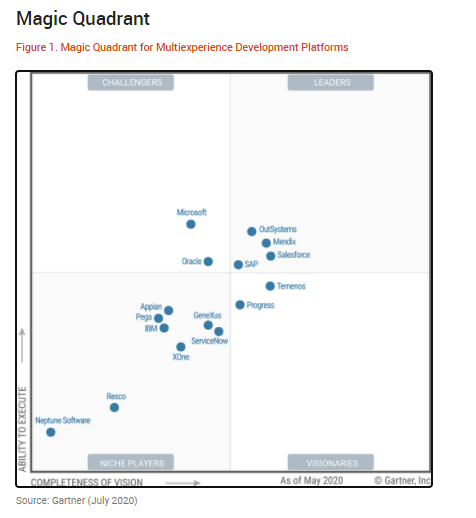

Going forward, I will anticipate more acquisitions to boost Progress’s competitive posture. The boost is required due to competition in other segments, such as the multi-experience development platforms (MXDPs) space. MXDP is a rising segment projected to grow due to the need for tools to develop web apps, chatbots, virtual reality, and IoT apps.

The improved caliber of its recent moves drives my conviction that Progress can find strong M&A candidates to boost its capabilities. I also believe it can negotiate attractive deals given the pandemic’s impact on startups with weak financials.

Valuation

Source: Seeking Alpha

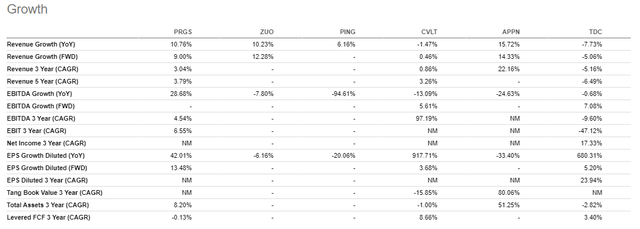

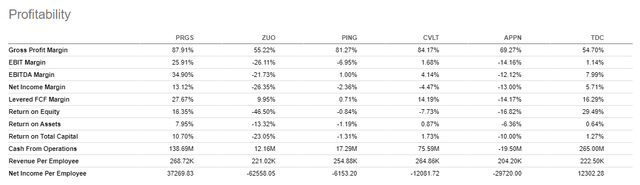

The acquisition of Chef is a boost to Progress’s valuation factors. This builds on the momentum from Ipswitch. Growth, Profitability, and Value are all solid. The growth grade is a blend of improved top-line and bottom-line (earnings) growth despite the headwinds from the pandemic.

Source: Seeking Alpha

Compared to its PaaS peers, Progress Software’s margins are impressive. TTM GAAP gross margin is the best amongst its peers. This is driving an A+ profitability grade, which flows all the way to the EBITDA margin line. The earnings growth and improved margins drive the value grade as its sales and earnings multiple remain attractive, given the weak momentum year to date.

I remain wary of the slow growth from the Data Connectivity segments in the near term. This is expected to be offset by new capabilities in other segments.

Data by YCharts

Data by YCharts

We anticipate operating margin for the year of approximately 40% with a slight Q4 headwind from the Chef acquisition. We are projecting adjusted free cash flow to be between $135 million and $140 million, an increase from our prior outlook. – Source – Q3’20 Earnings Call

Going forward, I expect a gradual improvement in the growth story. I am wary of the impact of acquisition-related expenses on its profitability factor. Regardless, I find Progress’s margins attractive, and the operating cash flow (adjusted FY guidance of $135m-$140m represents a margin of 30% using FY’20 revenue guidance of $452m-$456m) margin means Progress Software can easily raise more funds to achieve its M&A strategy. Since the cash flow margin affords management to acquire more growth options, I expect investors to have a more accommodative risk premium as the growth story unfolds. This will reduce Progress Software’s leverage ratios.

Source: Finbox

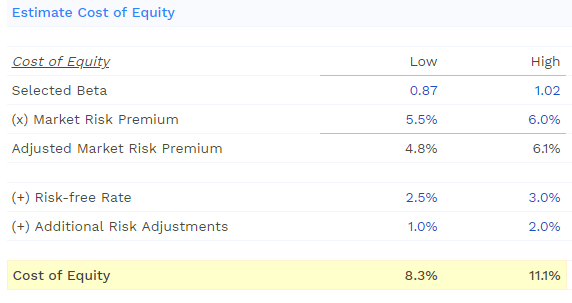

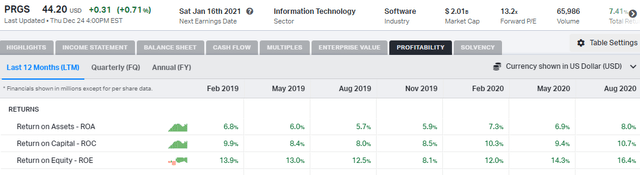

Since debt is a small portion of its total capital, I expect Progress Software’s discount rate to be driven by its cost of equity, which benefits from its improved ROE (return on equity).

Source: Koyfin

ROE has improved 31% y/y, and ROE margin stands at approx. 16% (using TTM net income of $57m and average shareholder equity of $327m). The improved ROE will drive low volatility as earnings assist growth.

Data by YCharts

Data by YCharts

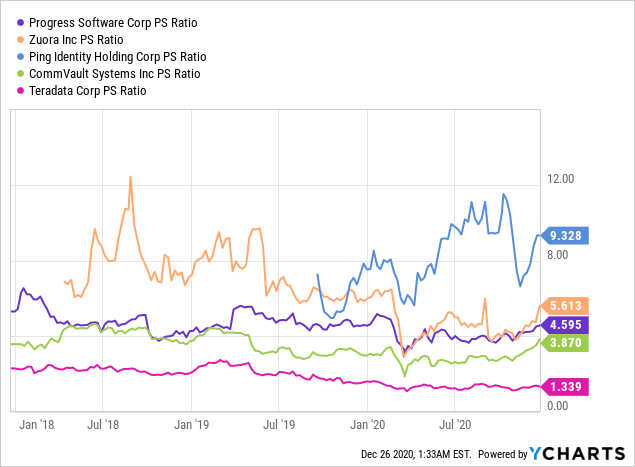

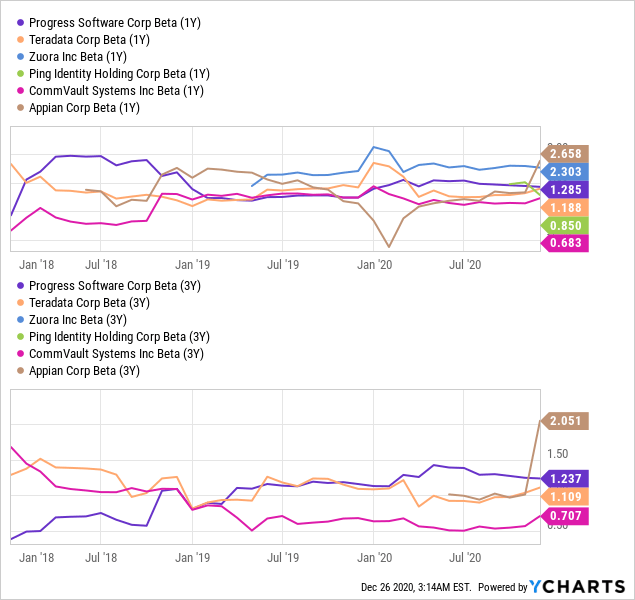

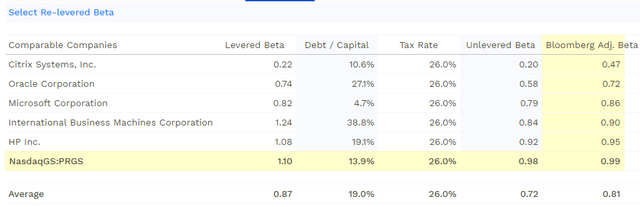

Compared to more volatile peers such as Zuora (NYSE:ZUO) and Teradata (NYSE:TDC), Progress has moderate trading volatility. Using a levered beta of 1.1-1.2 in line with the three-year average assuming 2021 is a less volatile year compared to the TTM beta (2020), we can derive the unlevered beta in the cost of equity table assuming a tax rate of 26% and debt to capital ratio of 14% (using debt of $320m and the current market cap of approx. $3b).

Source: Finbox

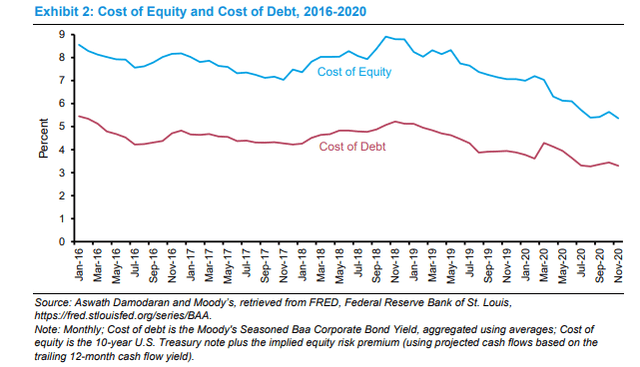

When computing the cost of equity, the low interest rate environment will drive a reduced risk-free rate and equity risk premium compared to the value used in the table above. This is supported by a recent paper from Morgan Stanley highlighting the recent decline in equity risk premium across equities due to the reduced yield on the 10-Y U.S. Treasury note, a good proxy for the risk-free rate.

Source: Morgan Stanley

Source: Morgan Stanley

By 2024, one in three enterprises will use a multi-experience development platform to increase the speed at which IT and business fusion teams work to deliver successful digital products. – Source – Gartner

My valuation assumes Progress maintains low-double-digit revenue growth over the next five years, driven by improved PaaS features. This includes an improved MXDP platform that will drive capabilities in VR/AR and IoT development tools. This growth will also derive from Chef’s positioning in DevSecOps.

After the next five years, I expect revenue growth to wane as low code platforms become more competitive. I also expect Progress to continue its strong cost management strategy to maintain an EBITDA margin above 30%. Since Capex/Sales has been historically lean at less than 2% of revenue, I expect Progress Software will maintain this reinvestment rate. Therefore, assuming FCF margin tracks EBITDA margin on strong earnings and working capital improvement, Using 18x exit FCF multiple (implied from perpetuity growth rate of 4% using Gordon growth model on exit FCF margin of 30%), we can derive a fair valuation which implies a 34% upside.

Source: Finbox

Risks

Progress’s growth momentum has been affected by the pandemic. If the macro environment doesn’t improve, growth might remain range-bound.

Competition in the MXDP space is strong. Progress was previously ranked as a leader in the MXDP space before slipping into the visionary bucket in the latest assessment. Gartner cited low visibility for its platform with more focus on small enterprises. I expect Progress to keep investing in new capabilities while boosting its market presence. The projected capabilities might impact its cash position and liquidity.

The case for multiple expansion assumes the current margins improvement will continue. If Progress is unable to sustain its cost optimization initiatives, its valuation might remain range-bound.

Conclusion

Progress’s improved growth strategy is worth studying. It has solid financials, given its attractive profit margins and cash flows. Its platform business model means it can tuck in new capabilities to improve its competitive posture. While the macro environment remains gloomy, I believe Progress can rebound in 2021, given its ample financial flexibility.

Disclosure: I/we have no positions in any stocks mentioned, and no plans to initiate any positions within the next 72 hours. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.